How To Choose The Right Retirement Plan For Your Small Business

Listen to the Talley Financial Podcast!

How to Choose The Right Retirement Plan for Your Small Business

By: David Talley, CFP®

One of the easiest opportunities for business owners and self-employed individuals to potentially lower their tax bill is to upgrade the type of retirement plan they have in place.

As businesses grow, they can outgrow their plan and end up paying more taxes than necessary because they’re not taking advantage of maxing out the right type of plan.

This guide aims to help point you in the right direction, but please consult a CPA or CFP knowledgeable about retirement plan design because there are factors to consider outside what’s presented here.

The key factors for determining the right business plan are:

- How much do the owners want to save?

- Does the business have employees?

- Is the retirement plan important for employee recruiting and retention?

Remember:

The plan you choose is mainly a tax planning decision. If you want to reach real financial independence, the assets inside these plans are the real driver of wealth.

Self-Employed

Traditional IRA, SEP IRA, Solo 401k, and Cash Balance Plan (2024)

Cheat Sheet:

| Plan Design |

Traditional IRA |

SEP IRA |

Solo 401k |

Cash Balance Plan |

| If you’d like to contribute: |

Less than $7k ($8k over age 50) |

More than $7k, but less than 25% of your net income |

More than 25% of your net income |

More than $100k every year |

Traditional IRA - If you want to contribute less than $7,000 ($8,000 over age 50).

- Defining features:

- Technically not a small business plan.

- Contributions don’t force employers to contribute to employee accounts.

- If you don’t have an employer-sponsored plan available from other employment, deduction is always allowed.

- Has a Roth option.

Traditional IRAs are a good fit for people starting their first retirement plan without a lot of money.

SEP IRA - If you’d like to contribute more than $7,000, but less than 25% of your net income.

- Defining features:

- Technically all contributions are profit sharing in nature, not salary deferrals.

- The employer’s contribution percentage is the same for all eligible participants.

- You can disallow any employee from participation in “profit sharing” if they have less than 36 months of employment (this is missed all the time!).

- Often a good plan for a small business with no employees or high employee turnover.

SEPs are generally a good fit for self-employed individuals who wish to save no more than 25% of their income each year and who don’t have any employees who are at least in their third calendar year of service.

Solo 401k - If you want to contribute more than 25% of your net income.

- Defining features:

- Max allowed contribution is $23,000 (salary deferral) plus 25% of your net income.

- Only available to only an owner or an owner and their spouse.

- You do have to pay a third-party plan administrator, but there are a ton of options under $100 annually

- Has a Roth option for the salary deferral portion of contributions.

For many self-employed individuals, a Solo 401k Plan is better than a SEP because the annual contribution limit is the “salary deferral” limit of $23,000 ($30,000 over age 50) plus 25% of eligible income. Whereas SEP IRAs (which are more common) only allow a contribution of 25% of eligible income.

Cash Balance Plan - If you want to contribute more than $100,000 (up to $3.6m) per year.

- Defining features:

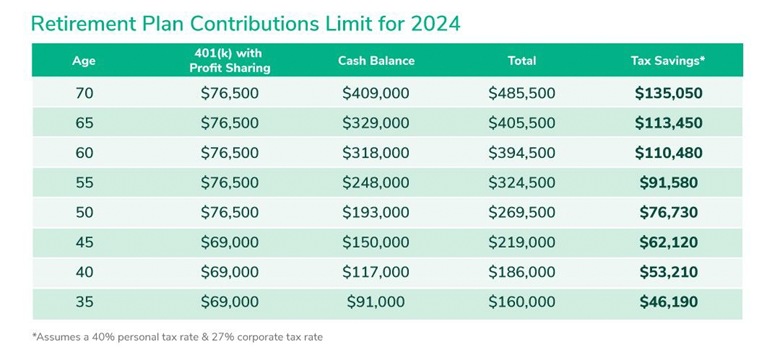

- Contribution limits are based on age. See 2024 table*

- Technically a hybrid “pension” plan that allows older participants to make larger contributions than other plans.

- Works best with few or no employees

- If you have employees, the larger the age gap, the better.

- More expensive than traditional plans because they require certification for proper funding. Administrative costs can range from $2-5k per year higher than a 401k.

- There’s funding flexibility via a “funding range,” but the employer’s required funding to the plan is consistent from year to year.

- Dependent on their ages, employer contributions for rank-and-file employees usually amount to roughly 7% compared with the 4.5% typical of 401(k) plans.

Small Business Plans

SEP IRA, SIMPLE IRA, 401k, and Cash Balance Plan

SEP IRA - If the owner has no employees with more than 3 years of work and wants to contribute more than $7,000 but less than 25% of their net income.

- Defining features:

- Technically all contributions are profit sharing in nature, not salary deferrals.

- The employer’s contribution percentage is the same for all eligible participants.

- You can disallow employees with less than 36 months of employment from “profit sharing.”(this is missed all the time!)

- A good plan for small businesses with one or two first-time employees or high employee turnover.

SEPs are generally a good fit for self-employed individuals who wish to save no more than 25% of their income each year and who don’t have any employees who are at least in their third calendar year of service.

SIMPLE IRA - If the owner wants to make retirement plan contributions for their employees and wants to save less than $22,000/year themselves.

- Defining features:

- Max employee contribution of $17,000 ($20,500 over age 50) per individual -plus- “employer” matching.

- Mandatory employer contribution. Either:

- Matching dollar for dollar up to 3%.

- Matching a flat 2% of employee compensation regardless of participation

- All contributions vest immediately.

- No Roth option

- No loans

- No annual tax filing requirements, so minimal fees/administration - often $0.

SIMPLE IRAs tend to be a good fit for business owners who want to provide a retirement plan for their employees in an easy, inexpensive manner and don’t want to make contributions over about $22,000 themselves.

Safe Harbor 401(k) Plan - If the owner wants to make retirement plan contributions for their employees and wants to save more than $22,000 each year themselves.

- Defining features:

- Max employee contribution of $23,000 ($30,500 for those over age 50) per individual -plus- employer matching up to a combined total of $61,000.

- Set up fees range from $1k-5k for most small businesses.

- Annual plan administrator fees range from $1k-3k for most small businesses.

- Roth option available

- Must adhere to top-heavy testing rules

- Allows for additional, discretionary “profit sharing” contributions, which can be made to favor business owners and can be subject to a vesting schedule for employees.

- Is more familiar to most workers than SEPs and SIMPLE IRAs.

Many business owners graduate from a SIMPLE IRA to a 401k when the business owners are committed to saving more than $22k per year and/or would like the option to make additional profit-sharing contributions to the owner and employees.

Cash Balance Pension Plan - If the owner would like to contribute more than $100,000 (up to $3.6m per year).

- Defining features:

- Contribution limits are based on age. See 2022 table.*

- Technically a hybrid “pension” plan that allows contributions far in excess of other plans for older participants.

- Works best with few or no employees

- If you have employees, the larger the age gap the better

- More expensive than traditional plans because they require certification to be properly funded. Administrative costs can range from $2-5k per year higher than a 401k.

- Although there is some funding flexibility via a “funding range,” the amount that the employer is required to fund to the plan is fairly consistent from one year to the next.

- Although dependent on their ages, employer contributions for rank-and-file employees usually amount to roughly 7% compared with the 4.5% that are typical of 401(k) plans only.

Cash Balance Plan 2024 Contribution Limits example:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

A Roth IRA offers tax deferral on earnings and tax-free qualified withdrawals. Withdrawals before age 59 ½ or before the account has been open for 5 years could result in a 10% IRS penalty tax. Limitations and restrictions may apply.